Key Takeaways for Newcomers

- "Temporary" in the USA often means a standard 6-month policy: True daily or weekly policies from major insurers are rare. Instead, newcomers typically purchase a standard policy and cancel early if needed, ensuring continuous coverage.

- International licenses are often accepted initially: Most U.S. states allow driving with a valid foreign license, sometimes with an International Driving Permit (IDP), for a temporary period before requiring a state-issued license.

- State laws vary significantly for immigrants: Some states are more accommodating, even allowing undocumented immigrants to obtain driver's licenses and, consequently, car insurance, making local research crucial.

Welcome to the United States! As you embark on this new chapter, navigating the complexities of daily life, including transportation, is a key step. Whether you're here for a short-term assignment, on a student visa, or making a permanent move, driving often becomes a necessity. Understanding how to secure temporary car insurance as a newcomer or immigrant in the USA is not just about convenience; it's a legal requirement in almost every state and crucial for your safety and financial protection.

The U.S. car insurance landscape can seem daunting, especially when your needs are temporary or you're unfamiliar with local regulations. Many assume "temporary" means easily acquiring a policy for just a few days or weeks. However, the reality is often more nuanced. This comprehensive guide will demystify temporary car insurance options, outline state-specific requirements, and provide actionable advice to help you get on the road legally and confidently.

Why Car Insurance is an Absolute Must in the USA

Unlike some countries, the vast majority of U.S. states mandate auto insurance for all drivers. Driving without proper coverage carries severe penalties, including hefty fines, vehicle impoundment, driver's license suspension, and even legal repercussions that could impact your immigration status. The primary purpose of this mandatory insurance is to ensure that drivers can cover the costs of damages or injuries they might cause in an accident.

For newcomers, this requirement can be particularly challenging. Your driving history from your home country may not be recognized, and you might not yet have a U.S. driver's license or credit history. These factors can influence the availability and cost of insurance. Therefore, securing adequate coverage from the outset is paramount, not only to comply with the law but also to protect yourself and others on the road.

Critical Warning: The Perils of Uninsured Driving

Driving without insurance in the U.S. is not only illegal but can also lead to devastating financial and legal consequences. In the event of an accident, you would be personally responsible for all damages, medical bills, and legal fees, which can quickly amount to hundreds of thousands of dollars. Always prioritize obtaining at least the minimum required coverage before driving.

Deciphering "Temporary" Car Insurance for Immigrants

The term "temporary car insurance" can be a source of confusion for many. In the U.S., major insurance providers generally do not offer standalone policies for periods shorter than six months. Instead, when newcomers speak of "temporary" coverage, they are often referring to several practical alternatives that fulfill short-term needs without requiring a long-term commitment.

These solutions are designed to bridge the gap until a more permanent driving and insurance solution is established. Understanding these options is key to making an informed decision that aligns with your specific situation and duration of stay in the U.S.

The Reality: Standard Policies with Flexibility

For most major insurers like Geico, State Farm, and Progressive, their shortest standard policy term is typically six months. However, the good news is that you can often purchase a standard six-month policy and cancel it early if your needs change. Many companies offer prorated refunds for the unused portion of your policy. This approach allows you to maintain continuous, valid insurance coverage for your desired period while providing the flexibility to end it without penalty (beyond a potential small cancellation fee).

Smart Strategy: Short-Term Standard Policies

If you anticipate needing coverage for a few months, consider purchasing a standard six-month policy. Before committing, inquire about the company's cancellation policy and whether they offer prorated refunds. This can be a straightforward way to ensure full compliance and coverage.

Tailored Short-Term Car Insurance Solutions for Newcomers

Depending on your unique circumstances—whether you're a short-term visitor, borrowing a friend's car, or establishing long-term residency—there are several effective strategies to obtain the necessary temporary car insurance.

1. Rental Car Insurance: Ideal for Short Visits

If you're visiting the U.S. for a few weeks or less and plan to rent a vehicle, purchasing insurance directly from the rental car company is often the most convenient and immediate solution. Rental agencies typically offer various coverage packages that meet state requirements. This includes:

- Liability Coverage: Protects you against costs if you cause damage or injury to others.

- Loss Damage Waiver (LDW) / Collision Damage Waiver (CDW): Covers damage to the rental car itself, often exempting you from financial responsibility.

- Personal Accident Insurance (PAI): Provides medical benefits for you and your passengers.

While rental car insurance can appear more expensive on a daily basis (ranging from $15-$50/day), it offers unparalleled ease and is perfect for truly short durations. Always check your credit card benefits, as some premium cards provide secondary rental car insurance coverage if you use them to book the vehicle.

2. Non-Owner Car Insurance: For Borrowed Vehicles

For newcomers who don't own a vehicle but frequently borrow cars from friends or family, or rent them occasionally, a non-owner car insurance policy is an excellent option. This type of policy provides liability coverage, protecting you if you're found at fault in an accident while driving a car you don't own. It helps maintain continuous insurance coverage, which can be beneficial for future rates.

Non-owner policies typically last for six months or a year and can be significantly cheaper than standard policies, as they don't cover a specific vehicle. Major insurers like State Farm and Progressive offer these policies, with costs often ranging from $200-$600 per year.

3. Being Added to an Existing Policy: A Collaborative Approach

If you're staying with friends or family and will be regularly driving their vehicle, the simplest solution might be for the policyholder to add you as a named insured or a temporary driver to their existing policy. Many insurance companies allow this, especially for household members. This ensures you are fully covered under their comprehensive auto insurance plan.

It's crucial to be transparent with the insurance company about who will be driving the car to avoid any issues in case of a claim. Be aware that adding a new driver, especially one without a U.S. driving history, might increase the policyholder's premiums.

4. Specialized Providers and International Plans

While less common, some specialty insurance providers cater specifically to expats, international students, or individuals with unique immigration statuses. Companies like Hallmark Financial Services (in certain states) or Clements Worldwide may offer more flexible or short-term plans tailored to international drivers. These options might be particularly useful if you find it challenging to obtain coverage from mainstream providers due to specific documentation or residency requirements.

Navigating Driver's License Requirements as a Newcomer

Your driver's license status is a cornerstone of obtaining car insurance in the U.S. Understanding the rules regarding international and state-issued licenses is vital.

International Driving Permit (IDP) and Foreign Licenses

- Initial Validity: Most U.S. states permit non-residents to drive with a valid foreign driver's license for a limited period, typically ranging from 30 days to one year.

- International Driving Permit (IDP): An IDP is a document that translates your foreign driver's license into multiple languages. While not a license itself, it is highly recommended as it validates your foreign license to U.S. authorities and rental car companies. It can extend your driving rights beyond what a foreign license alone might allow, often for up to a year.

- State Variations: The duration for which a foreign license is valid varies significantly by state. For instance, some states require you to obtain a local driver's license within a short period (e.g., 30-60 days) after establishing residency.

- Long-Term Residency: If you plan to reside in the U.S. long-term, you will eventually need to obtain a state-issued U.S. driver's license. This is a crucial step towards potentially lower insurance rates and full legal compliance.

Actionable Tip: Check Your State's DMV Regulations

Before driving, visit your specific state's Department of Motor Vehicles (DMV) website or office to understand the exact requirements for international drivers and the timeframe within which you must obtain a local license after becoming a resident.

Car Insurance for Undocumented Immigrants

Historically, obtaining a driver's license and car insurance as an undocumented immigrant in the U.S. was extremely challenging. However, this landscape is evolving, with several states now offering pathways to legal driving and insurance:

- State-Specific Licenses: As of early 2026, over 20 U.S. states and Washington D.C. permit undocumented immigrants to obtain a driver's license or a driving privilege card. These states include California, New York, Illinois, New Jersey, and others. This is a critical development, as a valid driver's license is typically a prerequisite for purchasing car insurance.

- Access to Insurance: In these states, once an undocumented immigrant obtains a valid driver's license, they can then purchase auto insurance from many major carriers. While initial rates might be higher due to the absence of a U.S. driving record or credit history, this ensures legal compliance and financial protection.

- Individual Taxpayer Identification Number (ITIN): For those without a Social Security Number (SSN), an ITIN can often be used for identification purposes when applying for a driver's license or insurance in states that allow it.

- DACA Recipients: Individuals with Deferred Action for Childhood Arrivals (DACA) status are generally eligible to obtain driver's licenses and, consequently, car insurance in most states.

States allowing undocumented immigrants to obtain driver's licenses. This map illustrates the expanding accessibility for newcomers.

Documentation You'll Need to Secure Coverage

To streamline the process of obtaining temporary car insurance, it's essential to have the following documents ready:

- Valid Driver's License: Your foreign driver's license, and an International Driving Permit (IDP) if you have one.

- Passport and Visa: Proof of your legal presence in the U.S.

- Proof of Address: A utility bill, lease agreement, or bank statement demonstrating your U.S. residency.

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN): While not always mandatory, having an SSN or ITIN can significantly simplify the process and potentially lead to better rates.

- Vehicle Information: If you've purchased a car, you'll need the Vehicle Identification Number (VIN), make, model, and year.

Comparing Top Insurers for Newcomers in the USA

Several major insurance companies are known for being accommodating to newcomers and immigrants, often accepting international driver's licenses and offering competitive rates. While "temporary" policies are rare, these providers offer standard policies that can be cancelled early, or specific solutions like non-owner insurance.

| Company | Best For | Starting Monthly Rate (Estimate) | Newcomer-Friendly Features | Short-Term Suitability |

|---|---|---|---|---|

| Geico | Competitive rates, online convenience | $35 - $50 | Accepts international licenses, easy online quotes, nationwide availability. | Standard 6-month policies (cancellable), non-owner policies. |

| State Farm | Personalized service, agent support | $40 - $60 | Accepts international licenses, large network of local agents for personalized assistance. | Standard 6-month policies (cancellable), non-owner policies, adding to existing policies. |

| Progressive | Flexible policies, discount programs | $45 - $65 | Accepts international licenses/IDPs, Snapshot program for potential discounts based on driving. | Standard 6-month policies (cancellable), non-owner policies, temporary additions. |

| Liberty Mutual | Same-day coverage options | $50 - $70 | Options for non-citizens, potential for same-day coverage, RightTrack safe-driving program. | Standard policies (cancellable), some short-term quote availability. |

| Hallmark Financial Services | Specific niche for foreign drivers | Varies widely | Specializes in temporary residents, international students, and workers with foreign licenses (in applicable states). | May offer more flexible short-term options depending on state. |

Note: These rates are estimates and can vary significantly based on your state, driving history, type of vehicle, coverage limits, and specific discounts. Always compare multiple quotes to find the best rate.

Factors Influencing Car Insurance Rates for Newcomers

Several variables impact your car insurance premiums, and some are particularly relevant to newcomers to the U.S.:

- Lack of U.S. Driving History: U.S. insurers generally cannot access driving records from other countries. This means you might be categorized as a "new driver," leading to higher initial rates.

- U.S. Credit History: In many states, insurance companies use credit scores as a factor in determining premiums. If you're new to the U.S. and haven't established a credit history, this can also result in higher rates.

- Driver's License Type: While foreign licenses and IDPs are accepted temporarily, obtaining a U.S. state-issued driver's license often leads to more favorable rates over time.

- Age and Marital Status: Younger drivers (under 25) typically pay more, and married individuals often receive discounts.

- Vehicle Type: The make, model, year, and safety features of your car significantly affect premiums.

- Location: Urban areas with higher traffic and theft rates usually have higher insurance costs than rural areas.

- Coverage Limits: Opting for higher liability limits or adding comprehensive and collision coverage will increase your premium but offer greater financial protection.

Smart Strategies for Saving on Temporary Coverage

Even with the unique challenges faced by newcomers, there are several ways to potentially reduce your car insurance costs:

- Compare Multiple Quotes: This is the single most effective way to find affordable coverage. Rates vary significantly between insurers, so get quotes from at least three different companies.

- Inquire About Discounts: Many insurers offer various discounts that you might qualify for, such as:

- Safe driver programs (telematics devices that monitor driving behavior)

- Bundling (e.g., combining auto with renter's insurance)

- Paying premiums in full or opting for electronic payments

- Good student discounts (for international students)

- Choose Appropriate Coverage: While full coverage is ideal, if you're driving an older, less valuable vehicle, you might consider foregoing comprehensive and collision coverage to save money. Always ensure you meet your state's minimum liability requirements.

- Maintain a Clean Driving Record: Over time, a clean U.S. driving record will be your best asset for reducing premiums. Drive safely and avoid tickets or accidents.

- Consider Usage-Based Insurance: If you don't drive frequently, programs like Progressive's Snapshot or State Farm's Drive Safe & Save can offer discounts based on your actual driving habits.

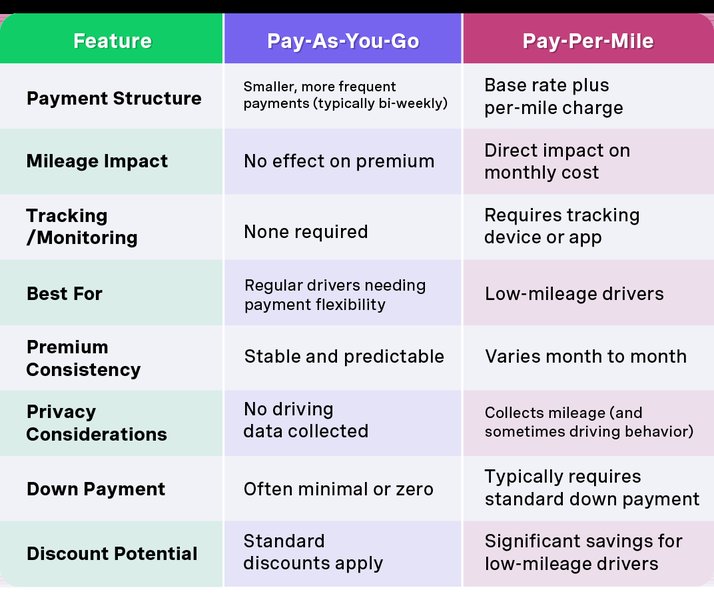

Infographic illustrating Pay-As-You-Go vs. Pay-Per-Mile insurance models, which can help reduce costs for infrequent drivers.

Did You Know? Building a U.S. Driving Record

Even if your international driving record was spotless, U.S. insurers often treat you as a new driver. This can lead to rates that are 10-30% higher initially. However, your rates will typically decrease as you establish a clean U.S. driving record over time. Patience and safe driving pay off!

Common Misconceptions About Car Insurance for Immigrants

Navigating a new country's legal and financial systems comes with its share of myths. Let's debunk some common misunderstandings about car insurance for newcomers:

- Myth: My car insurance from my home country automatically covers me in the U.S.

- Reality: Generally, international car insurance policies do not extend coverage to the U.S. While Canadian drivers may have limited cross-border coverage, most international visitors will need to secure a U.S.-based policy or specific rental car insurance.

- Myth: You can easily find genuine daily or weekly car insurance policies from major providers.

- Reality: As discussed, major U.S. insurers primarily offer policies with a minimum term of six months. Be wary of unverified providers offering extremely short-term policies, as they might be scams or provide insufficient coverage.

- Myth: Insurers will recognize my excellent driving history from my home country.

- Reality: Unfortunately, U.S. insurance companies typically cannot access international driving records. You will often be rated as a new driver in the U.S., which means your initial rates might be higher regardless of your past experience.

- Myth: Undocumented immigrants cannot get car insurance in any U.S. state.

- Reality: This is increasingly false. A growing number of states allow undocumented immigrants to obtain driver's licenses, which then enables them to purchase car insurance and drive legally.

Making Your Transition Smooth: A Step-by-Step Approach

Securing temporary car insurance as a newcomer doesn't have to be overwhelming. Follow these steps for a smooth process:

- Understand Your Needs: Determine how long you need coverage and what type of driving you'll be doing (renting, borrowing, or owning).

- Research State Requirements: Check your specific state's DMV website for driver's license regulations for international visitors and new residents, as well as minimum insurance requirements.

- Gather All Documents: Compile your foreign driver's license, IDP, passport, visa, proof of address, and SSN/ITIN if available.

- Get Multiple Quotes: Contact several major insurers (Geico, State Farm, Progressive, Liberty Mutual) and any specialized providers. Use online quote tools or speak directly with agents.

- Inquire About Discounts: Always ask about potential discounts for which you might be eligible.

- Purchase Your Policy: Once you've compared options and found the best fit, purchase your policy. Many companies offer same-day coverage.

- Obtain Your State License (if applicable): If you plan to stay long-term, prioritize obtaining your state-issued driver's license within the required timeframe to potentially reduce future insurance costs.

"When I first arrived in California from India, I was worried about getting car insurance. I called a local State Farm agent, and they walked me through the process, even accepting my international license initially. It made a huge difference!"

— Priya S., Los Angeles Resident

Frequently Asked Questions (FAQ)

Conclusion: Driving Legally and Confidently

Navigating the U.S. car insurance system as a newcomer or immigrant requires a bit of research and understanding, but it is entirely achievable. The key is to recognize that "temporary car insurance" often translates to flexible standard policies, rental car coverage, or non-owner policies that cater to your short-term needs. By understanding state-specific requirements, gathering the necessary documentation, and comparing quotes from reputable providers, you can secure the coverage you need to drive legally and with peace of mind.

Remember, driving without insurance is a significant risk with severe consequences. Taking the proactive steps outlined in this guide will not only keep you compliant with U.S. laws but also protect your finances and ensure a smoother transition into your new life in America. Welcome to the U.S. – and happy, safe driving