Discover how location-specific factors, from specialized repair networks to regional accident rates, profoundly shape what you pay for Tesla coverage.

Highlights

- Location-Specific Repair Costs: Tesla's unique design and reliance on a limited network of certified repair shops mean that the proximity and density of these facilities in your ZIP code heavily influence insurance premiums.

- Dynamic Risk Assessment: Insurers evaluate local accident rates, theft statistics, and even environmental risks to determine your Tesla insurance cost by ZIP code, leading to significant variations between urban and rural areas, and across states.

- Tesla Insurance's Alternative Model: Tesla's in-house insurance product offers a distinctive approach, often prioritizing real-time driving behavior (Safety Score) over traditional geographic risk factors, potentially offering savings for safe drivers in high-cost areas.

Your ZIP code is far more than just a mailing address when it comes to insuring a Tesla. Unlike conventional vehicles, Teslas have specific requirements for repair and maintenance that are deeply tied to geographic availability and local economic conditions. This means that your tesla insurance quote is acutely sensitive to where you live, reflecting everything from the density of Tesla-certified repair shops to regional accident frequency and parts availability. Understanding these localized influences is crucial for both prospective and current Tesla owners navigating the landscape of premiums.

The Unique Interplay of Location and Tesla Insurance Premiums

While location always plays a role in car insurance, its impact on Tesla premiums is significantly amplified. This heightened sensitivity stems from the advanced technology, specialized materials (like aluminum frames), and intricate software systems inherent to every Tesla. These elements demand highly specialized tools, rigorous training, and genuine Original Equipment Manufacturer (OEM) parts for any repair, even minor ones. The availability and cost of these critical resources can vary dramatically by ZIP code and state, directly translating into fluctuating insurance rates.

Why Tesla Insurance is Expensive by Location: The Repair Network and Parts Conundrum

One of the primary drivers behind location-sensitive Tesla insurance premiums is the brand's restricted network of authorized repair facilities. This limited access means that in many areas, there are fewer options for servicing a damaged Tesla, potentially leading to longer repair times and higher labor costs. Insurers meticulously factor these increased expenses into their premium calculations.

Specialized Repair Requirements

- Advanced Technology: Teslas are equipped with sophisticated features, including numerous Autopilot sensors, cameras, and integrated structural battery packs. Even a seemingly minor fender bender can necessitate complex diagnostics and repairs to these high-tech components, often exceeding the repair costs of a traditional internal combustion engine (ICE) vehicle.

- Genuine OEM Parts: Tesla-approved body shops are mandated to use only genuine Tesla parts. The proprietary nature and often limited availability of these components mean higher acquisition costs for repair centers, which are then passed on to insurers and, consequently, to policyholders. For instance, replacing a Tesla battery can be a substantial expense, ranging from $13,000 to over $20,000.

- Certified Technicians: Repairing a Tesla is not a job for any mechanic. It requires technicians who have undergone specific, rigorous training and certification directly from Tesla. The scarcity of such highly specialized individuals in certain geographical areas contributes to elevated labor costs. Many reputable collision centers, like Fix Auto USA locations, achieve I-CAR Gold Class and Tesla certifications to meet these demanding standards.

The density of these Tesla-certified collision centers directly influences premiums. States or ZIP codes with a higher concentration of certified shops generally experience more efficient repair processes and potentially more competitive pricing, which can lead to lower insurance costs. Conversely, areas with fewer authorized facilities often face increased logistics, such such as longer towing distances, extended repair durations, and higher overall costs for insurers.

A visual representation of Tesla-certified body shop density across various regions.

Tesla Insurance Cost by ZIP Code and State: A Granular Perspective

The exact street where your Tesla is garaged, down to its specific ZIP code, is a pivotal factor in determining your insurance premium. Urban areas, characterized by higher population densities, increased traffic congestion, and often elevated crime rates, typically incur steeper premiums due to a greater statistical likelihood of accidents and theft. In contrast, more rural regions may offer lower rates, although risks like wildlife collisions or extended emergency response times can still influence coverage choices.

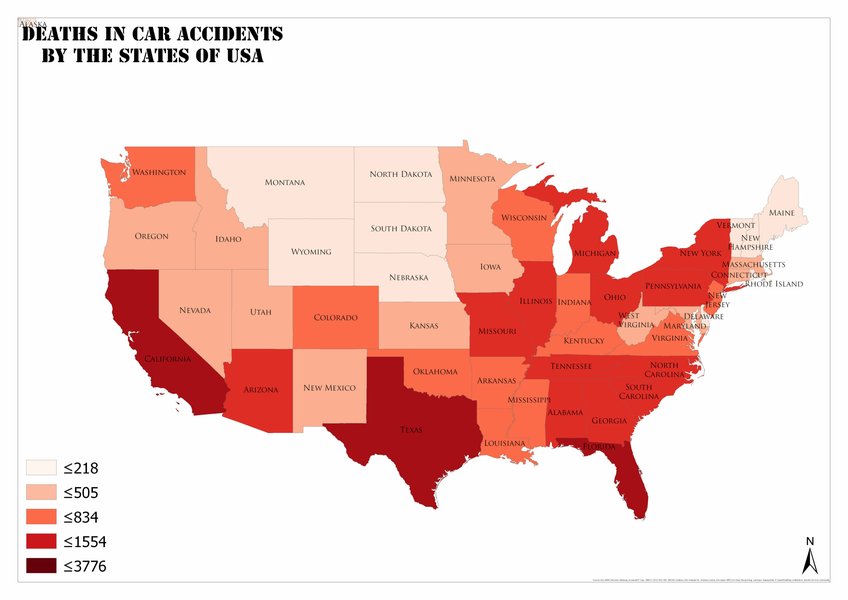

Tesla Insurance Rates by State 2026: Navigating the Cost Spectrum

Insurance rates for Teslas exhibit considerable variation across the United States. Factors such as state-specific insurance regulations, local traffic laws, weather patterns, and the overall cost of living all contribute to this disparity. Here's a comparative overview of estimated average annual full coverage rates for Teslas, providing insight into the most and least expensive states:

| State (Most Expensive) | Estimated Annual Cost | Key Contributing Factors |

|---|---|---|

| Louisiana | $5,718+ | High accident rates, robust litigation environment, natural disaster risks, potentially fewer certified repair shops. |

| Michigan | $5,447+ | No-fault insurance laws, higher claim rates, elevated urban traffic. |

| California | $5,257+ | High cost of living, dense urban traffic, high repair labor costs, strict regulations limiting telematics. |

| New York | $4,573+ | Extreme population density, high urban traffic, elevated repair labor costs. |

| Florida | $4,400+ | Frequent natural disaster risks (hurricanes), high urban density, no-fault laws, high uninsured motorist rates. |

| State (Cheapest) | Estimated Annual Cost | Key Contributing Factors |

| Vermont | $2,400+ | Lower population density, fewer claims, less complex road systems, favorable state regulations. |

| North Carolina | $2,300+ | Lower accident rates, competitive insurance market, generally lower cost of living. |

| Maine | $2,800+ | Low population density, fewer claims, less urban congestion. |

| Ohio | $2,650+ | Generally lower overall insurance costs, competitive market, moderate risk factors. |

| Iowa | $2,500+ | Very low population density, minimal urban congestion, lower accident rates. |

Important Note: These figures represent estimated averages for full coverage. Individual rates are highly dependent on the specific Tesla model, driver profile, chosen coverage selections, and the particular insurer. City-level differences within each state can be even more pronounced.

How Location Affects Car Insurance Premium: Urban vs. Rural Dynamics for Teslas

The distinction between urban and rural environments significantly impacts premiums, especially for Teslas. Urban settings like Los Angeles, New York City, or Miami tend to have higher insurance rates for Teslas due to:

Urban Pressures

- Higher Accident Frequency: Increased traffic density and more complex road systems lead to a greater number of collisions.

- Elevated Vandalism and Theft: Densely populated areas often correlate with higher crime statistics, including vehicle theft and vandalism, which are factored into comprehensive coverage costs.

- Costly City Repairs: Even minor incidents in urban settings can easily damage advanced sensors and cameras, necessitating expensive calibration and replacement of proprietary parts. High urban labor rates further inflate these costs.

Conversely, rural drivers might benefit from lower premiums due to:

Rural Advantages and Challenges

- Lower Accident Rates: Less traffic generally means fewer collisions.

- Reduced Theft Risk: Rural areas typically experience lower rates of vehicle theft and vandalism.

- Repair Logistics: While frequency is lower, the scarcity of Tesla-certified shops in rural areas can lead to higher costs due to longer towing distances, extended repair times, and increased vehicle transportation expenses, potentially offsetting some savings.

An infographic illustrating the impact of urban vs. rural locations on Tesla insurance, highlighting common risk factors.

Accident and Theft Rates by ZIP Code: Direct Impact on Tesla Premiums

Local accident and theft statistics are direct inputs into an insurer's premium rating models. If your neighborhood, identified by its ZIP code, has historically high rates of collisions, bodily injury claims, or comprehensive losses (theft, vandalism, severe weather), these trends will result in higher premiums for all residents in that area, regardless of individual driving records.

Tesla-Specific Claim Cost Drivers

- Sensor and Camera Damage: Even low-speed impacts can damage critical Autopilot sensors and cameras, requiring expensive recalibration or replacement.

- OEM Component Costs: Replacing components like specialized glass, aluminum body panels, or battery-adjacent parts is significantly more expensive than for traditional vehicles.

- Calibration and Scan Requirements: Post-collision repairs often require specific OEM procedures for diagnostic scans and recalibration of Advanced Driver-Assistance Systems (ADAS), adding to the complexity and cost.

- Parts Scarcity: Delays in receiving proprietary Tesla parts can lead to extended rental car usage and storage fees, further increasing the overall claim cost.

Tesla Insurance: A Distinct Approach to Pricing Premiums

Tesla's own insurance product offers a unique alternative to traditional carriers, fundamentally altering how premiums are calculated. Available in select states (including Arizona, California, Colorado, Florida, Illinois, Maryland, Minnesota, Nevada, Ohio, Oregon, Texas, Utah, and Virginia), Tesla Insurance uses a real-time monitoring system called "Safety Score" to assess driving behavior. This means your insurance premium can adjust monthly based on your actual driving habits, alongside factors like the Tesla model, garaging address, and miles driven.

Key Differentiators of Tesla Insurance

- Telematics-Driven Pricing: In most eligible states, the Safety Score, derived from data collected directly from your vehicle, is a primary determinant of your monthly premium. Safe driving can significantly offset higher location-based risk factors.

- Integrated Coverage: Tesla Insurance offers standard coverages with a deep understanding of Tesla's specific repair needs, ensuring alignment with OEM standards and calibration requirements.

- No Additional Hardware: Unlike many telematics programs, Tesla Insurance leverages the vehicle's built-in sensors, eliminating the need for separate tracking devices.

Pro Tip: If you reside in a high-cost ZIP code, maintaining an excellent Safety Score with Tesla Insurance could lead to substantial savings compared to static rates from traditional insurers who rely more heavily on generalized location data. However, be aware that in states like California, regulatory restrictions currently limit telematics-based pricing for Tesla Insurance, basing rates on traditional actuarial factors instead.

Practical Strategies to Reduce Location-Based Tesla Insurance Costs

Even if you live in an area with historically high premiums, several proactive steps can help mitigate your tesla insurance cost by zip code:

Smart Shopping and Policy Adjustments

- Shop Multiple Providers: Rates vary significantly between insurers. Obtain quotes from at least 4-5 different carriers, including major providers like State Farm, GEICO, Nationwide, Progressive, and Tesla Insurance itself.

- Increase Deductibles: Opting for higher deductibles on your comprehensive and collision coverage can lower your monthly or annual premium. Ensure you have sufficient savings to cover the higher out-of-pocket expense if a claim arises.

- Bundle Insurance Policies: Combining your auto insurance with homeowners, renters, or umbrella policies through the same provider often unlocks significant multi-policy discounts.

- Clarify Coverage: Always confirm that your policy specifically covers OEM parts and ADAS calibration according to Tesla's specifications.

Vehicle and Usage Optimization

- Maintain a Clean Driving Record: A history free of accidents and violations is universally recognized by insurers as a key indicator of lower risk, leading to better rates.

- Utilize Safety Features: Ensure all your Tesla's advanced safety features (Autopilot, automatic emergency braking, etc.) are active and correctly calibrated. Some insurers offer discounts for these systems.

- Secure Parking: Parking your Tesla in a locked garage, especially in high-theft areas, can reduce the risk of theft or vandalism, potentially lowering comprehensive coverage costs.

- Consider Tesla Insurance (if applicable): If available in your state, focus on maintaining a high Safety Score to maximize potential savings.

- Accurate Mileage Reporting: If you drive less than the average, ensure your insurer has an accurate estimate of your annual mileage, as lower mileage often correlates with lower risk.

Is Relocation Worth It for Cheaper Tesla Insurance?

Moving solely for the purpose of reducing car insurance premiums is generally impractical for most individuals. While the difference in annual premiums between certain states or ZIP codes can indeed be significant—potentially $1,000 to $2,500 or more—the financial and logistical burdens of relocation (moving costs, changes in housing expenses, job commutes, taxes, etc.) typically outweigh the potential insurance savings.

When Relocation Might Make Financial Sense

- Already Planning a Move: If you are already considering relocating for other reasons (job change, family, lifestyle), investigating the average Tesla insurance costs in prospective areas should be a critical part of your research.

- Shifting from High-Risk Urban to Safer Suburbs: Moving from a high-loss urban ZIP code to a statistically safer, nearby suburban area within the same state might yield noticeable premium reductions without a drastic lifestyle upheaval.

- Improved Repair Access: Relocating to an area with a higher density of Tesla-certified repair facilities and more competitive labor rates could contribute to long-term savings on both repair costs and insurance premiums.

Frequently Asked Questions (FAQ)

Conclusion

The journey to understanding your tesla insurance quote is intrinsically linked to your geographic location. The unique characteristics of Tesla vehicles—their advanced technology, reliance on specialized repair networks, and proprietary parts—mean that traditional geographic risk factors are amplified. From the density of Tesla-certified shops to local accident and theft rates, your ZIP code is a powerful determinant of your premium. While these factors can lead to higher costs in certain areas, proactive steps like shopping multiple providers, optimizing driving habits with Tesla Insurance, and bundling policies can help manage expenses. For those considering a Tesla, or current owners looking to optimize their premiums, a thorough understanding of these location-based dynamics is indispensable.